Factor pricing , marginal productivity theory , modern theories of wage and interest and profit..for 11th,12th , B.Com. and B.A. unit 5

The theory of factor pricing -

The theory of factor pricing, also known as the theory of distribution, is an economic concept that explains how various factors of production are compensated for their contributions to the production process. The key factors of production are typically land, labor, and capital. Here are some key principles:

1. Marginal Productivity Theory:- This theory suggests that the price or income a factor receives is determined by its marginal productivity. In other words, factors of production are paid according to the additional value they contribute to the production process.

2. Marginal Revenue Product:- Factors are compensated based on the marginal revenue product they generate. If an additional unit of a factor increases total revenue, then it's worth more.

3. Perfect Competition:- In perfectly competitive markets, factors of production will earn the value of their marginal product. This is the most efficient allocation of resources.

4. Imperfect Competition:- In real-world situations, factors may not be paid exactly what they contribute due to various market imperfections, such as monopoly power or information asymmetry.

5. Wage Determination:- For labor, factors affecting wages include skills, education, experience, and demand for certain types of labor in the market.

6. Interest Rates and Capital :- The price of capital (interest rates) is determined by factors such as the supply of savings and the demand for investment.

7. Rent for Land and Natural Resources:- Rent for land is determined by factors like location, fertility, and scarcity.

The theory of factor pricing helps to understand how resources are allocated in an economy and how the rewards for factors of production are determined based on their contribution to the production process.

Marginal productivity theory detailed explanation -

The Marginal Productivity Theory of Distribution is a key concept in economics that explains how the income or distribution of earnings to factors of production, such as labor and capital, is determined in a competitive market. This theory is closely associated with the work of economists like John Bates Clark and Alfred Marshall. Here are the key points of the theory:

1. **Marginal Productivity**: According to this theory, the income that a factor (e.g., labor or capital) receives is equal to its marginal productivity. In other words, each factor is paid based on the additional output it contributes to the production process.

2. **Diminishing Marginal Returns**: The theory assumes that as more units of a factor are added to the production process while keeping other factors constant, the additional output (marginal product) of that factor will eventually diminish. This is known as the law of diminishing marginal returns.

3. **Equilibrium in Competitive Markets**: In competitive markets, factors of production are paid their marginal product because firms seek to maximize profits. If a factor is paid less than its marginal product, firms have an incentive to hire more of that factor, and if paid more, they have an incentive to hire less.

4. **Fair Compensation**: The theory suggests that in a competitive market, factors of production are compensated fairly based on their contribution to production. Therefore, wages, rents, and interest rates are seen as just and efficient.

5. **Real-World Limitations**: While the theory provides a useful framework for understanding income distribution, it simplifies many real-world complexities, such as imperfect competition, information asymmetry, and non-identical factors, which can affect how factors are compensated.

Overall, the Marginal Productivity Theory of Distribution is a foundational concept in economics that helps explain how factors of production are rewarded in a market economy. It's based on the idea that in a competitive market, factors are paid according to their contribution to the production process.

Modern theories of wage -

Modern theories of wages have evolved to address the complexities of labor markets, considering factors like human capital, labor market imperfections, and wage inequality. Here are some modern theories of wages:

1. **Human Capital Theory**: This theory, associated with economists like Gary Becker, emphasizes that wages are determined by an individual's investment in education, skills, and training. It suggests that individuals with more human capital (knowledge and skills) earn higher wages due to their increased productivity.

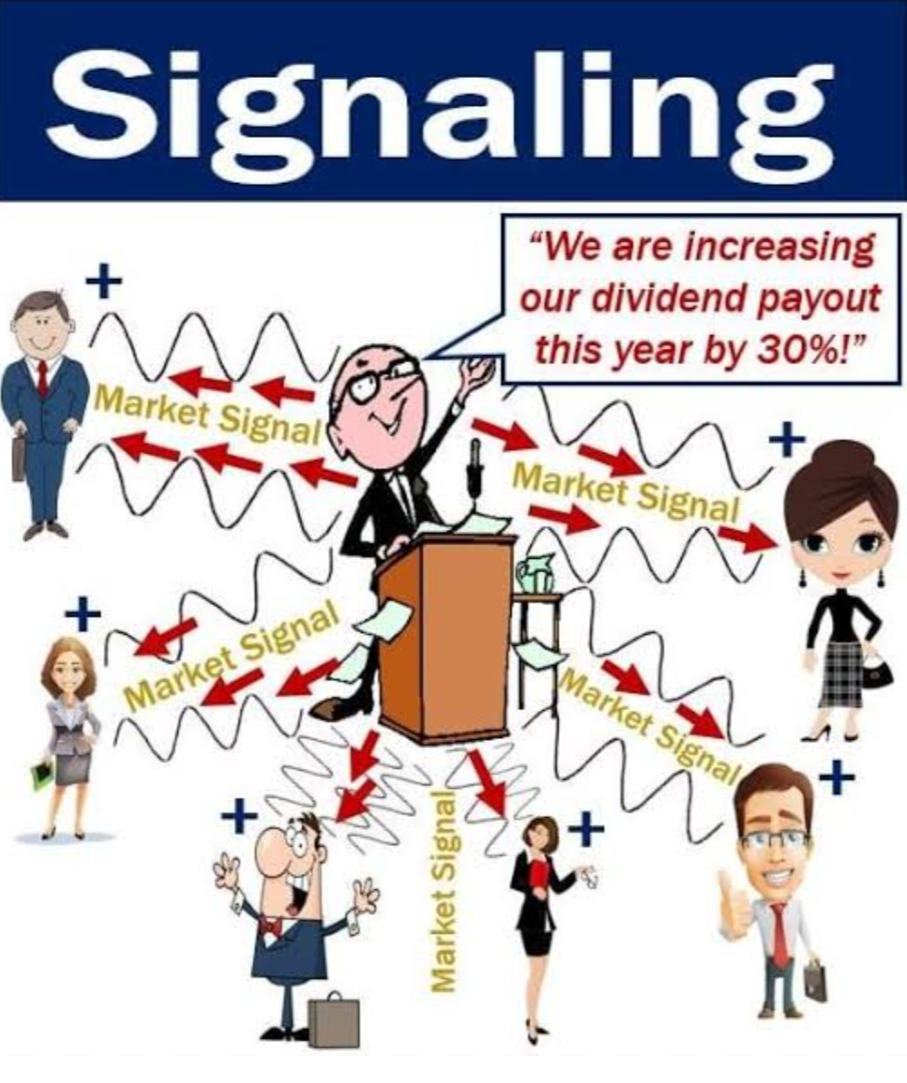

2. **Signaling Theory**: Michael Spence's signaling theory argues that education serves as a signal to employers, indicating an individual's ability and suitability for a job. People with higher levels of education may earn higher wages because they signal their skills and commitment to potential employers.

3. **Efficiency Wage Theory**: Proposed by economists like George Akerlof and Joseph Stiglitz, this theory suggests that paying wages above the market equilibrium can lead to increased productivity and reduced turnover. Employers may pay higher wages to motivate workers and reduce shirking.

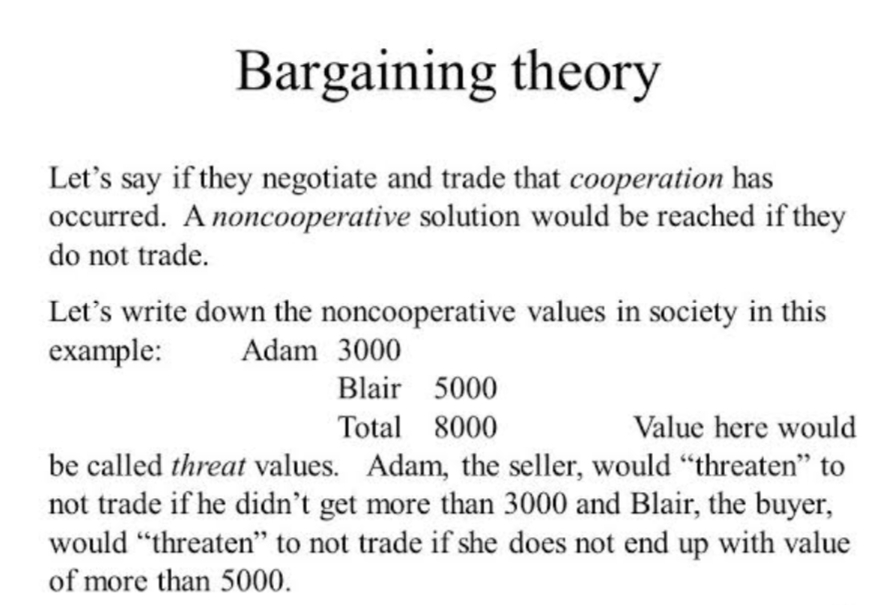

4. **Bargaining Theory**: This theory, associated with John Dunlop and others, emphasizes the role of labor unions and collective bargaining in wage determination. It suggests that wages are influenced by the negotiation power of workers and unions.

5. **Job Matching and Search Theory**: Economists like Peter Diamond and Dale Mortensen developed job matching and search theory, which explains that wages can be influenced by the time and effort it takes for job seekers and employers to find the right job-employee match. This can affect wage differentials.

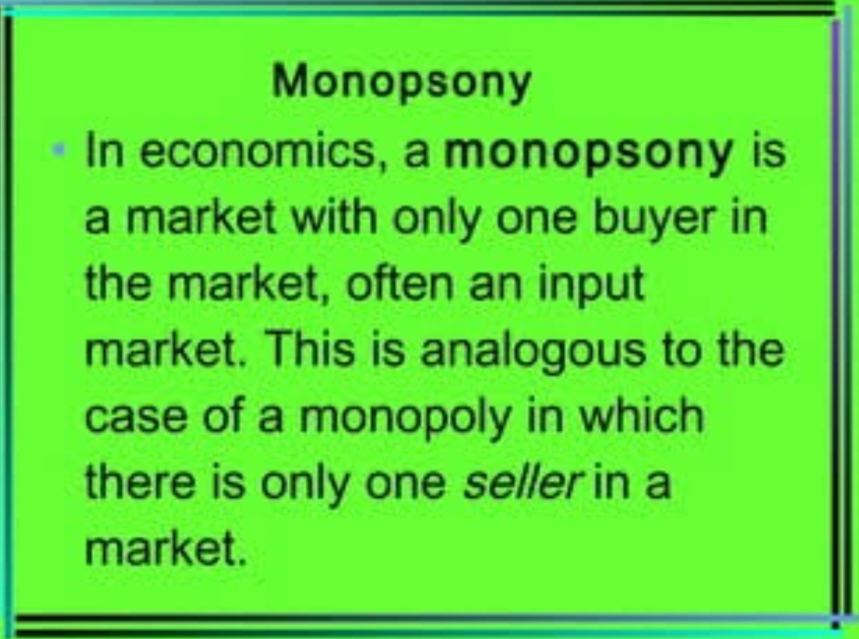

6. **Monopsony Theory**: Monopsony occurs when a single buyer (employer) dominates a labor market. Joan Robinson's monopsony theory suggests that employers in such situations can exert downward pressure on wages, leading to suboptimal wage levels.

7. **Wage Inequality Theories**: Various modern theories address wage inequality, including the skill-biased technological change theory, which argues that technological advancements increase the demand for high-skilled workers, leading to wage disparities.

8. **Minimum Wage Theory**: The debate surrounding minimum wage policies explores the impact of government-mandated wage floors on labor markets. Supporters argue that it can raise incomes for low-wage workers, while opponents suggest it may lead to job loss.

Modern theories of wages consider a wide range of factors, including education, skills, market imperfections, and the broader economic context, in explaining how wages are determined and why wage disparities exist in the labor market.

Interest and profit -

Interest and profit are two distinct financial concepts:

1. Interest:

- Interest is a fee or charge paid by a borrower to a lender for the use of borrowed money. It is typically calculated as a percentage of the principal amount borrowed and is paid over a specified period, often as part of a loan or credit agreement.

- Interest can be fixed or variable, and it serves as a reward to the lender for providing funds and as a cost to the borrower for using those funds. Common examples of interest include the interest on savings accounts, mortgages, and personal loans.

2. Profit:

- Profit, on the other hand, refers to the financial gain or benefit obtained by a business or individual after deducting all expenses, costs, and taxes from the revenue generated. It's the surplus left over when income exceeds expenditures.

- Profit can come from various sources, such as selling goods or services, investing in stocks, or running a business. It represents the positive financial outcome of an economic activity.

In summary, interest is a cost or revenue associated with borrowing or lending money, while profit is the overall financial gain achieved after accounting for all costs and expenses in a business or investment.

Done by Rohit Joshi.....

Also read this ...

Comments

Post a Comment