what is Microeconomics -

Microeconomics is the social science that

studies the implications of human action,

specifically about how those decisions affect the utilization and distribution of scarce resources. Microeconomics shows how and why different goods have different values, how individuals make more efficient or more productive decisions, and how individuals best

coordinate and cooperate with one another.

"Generally speaking, microeconomics İs

considered a more complete, advanced, and settled science than macroeconomics

Microeconomics is the study of economic

tendencies, or what is likely to happen when individuals make certain choices or when the factors of production change. Individual actors are often grouped into microeconomic subgroups, such as buyers, sellers, and business Owners. These groups create the supply and demand for resources, using money

and interest rates as a pricing mechanism for cOordination.

Nature of microeconomics -

Microeconomics represents the study of how members in a society use available resources to make choices in the marketplace. Those choices refer to purchases of goods and services from business providers. As business, part of your role is to provide and promote products that are demanded by a

target market group within the population. In essence, you want to influence the choices of consumers who have limited budgets to spend on various products and services

(1) supply and demand -

Supply and demand is one of the most critical.concepts at the microeconomic level. This is the comparison of the level of consumer demand for particular goods to the available supply in the marketplace. In a highly competitive industry in which Consumers possess many choices, supply might exceed demand. Over time, this can cause some businesses to fail. In a more niche market with few providers, your opportunity to succeed in meeting demand may be higher if you offer and

promote a quality product with desired bernefits.

(2) pricing -

Business pricing strategies correlate strongly with microeconomic factors. The ideal, or equilibrium price point exists at the point at which quantity supplied in the market exactly equals demand. The higher your prices, the lower the size of the population who wil| buy them. However, if you offer lower prices than the market demand dictates, you leave money on the table and you might also end up with shortages of your product or services. This can cause customer alienation and negatively affect the business in the long term.

(3) research and promotion -

Understanding microeconomics helps in

effectively researching and products. Research is useful in investigating

potential customer demand and in developing products that best match desired benefits. This benefits you once you pay for advertising and use other promotional techniques to promote

your brand and its benefits. These marketing techniques are critical in achieving competitive advantages over other companies trying to optimize performance as customers make choices based on their needs and budgets promoting .

Scopes of microeconomics -

The scope or the subject matter of microeconomics is concerned with -

(i) Commodity pricing

The price of an individual commodity is

determined by the market forces of demand and supply. Microeconomics is concerned with demand analysis i.e. individual consumer behavior, and supply analysis i.e. individual producer behavior.

(ii) Factor pricing theory

Microeconomics helps in determining the

factor prices for land, labor, capital, and

entrepreneurship in the form of rent, wage,

interest, and profit respectively. Land, labor, capital, and entrepreneurship are the factors that contribute to the production process.

(ii) Theory of economic welfare

Welfare economics in microeconomics is

concerned with solving the problems in

improvement and attaining economic efficiency to maximize public welfare. It attempts to gain efficiency in production,

consumption/distribution to attain overall

efficiency and provides answers for What to produce?, When to produce?', How to

produce?, and 'For whom it is to be produced?'

Equilibrium

KEY TAKEAWAYS

• Economic equilibrium is a

condition where market forces are

balanced, a concept borrowed

from physical sciences, where

observable physical forces can

balance each other.

• The incentives faced by buyers and

sellers in a market, communicated

through current prices and

quantities drive them to offer

higher or lower prices and

quantities that move the economy

toward equilibrium.

• Economic equilibrium is a

theoretical construct only. The

market never actually reaches

equilibrium, though it is constantly

moving toward equilibrium.

Dynamic equilibrium and static Equilibrium -

What ls Dynamic Equilibrium

Dynamic equilibrium in microeconomics refers to a situation where market conditions are constantly changing, but prices and quantities in the market tend to adjust over time to maintain a state of balance or equilibrium. This concept takes into account the fact that supply and demand are not static, and they can fluctuate due to various factors, such as changes in consumer preferences, technology, or external events.

In dynamic equilibrium, markets are continuously adjusting to new information and changes in the environment. For example, if demand for a product increases, prices may rise, encouraging more producers to enter the market. As they do, supply increases, which can eventually lead to a new equilibrium with higher quantities and prices.

Overall, dynamic equilibrium recognizes that economic systems are in a constant state of flux, with supply and demand responding to these changes, eventually settling into a new equilibrium that reflects the altered market conditions.

What is static equilibrium -

Static equilibrium in microeconomics refers to a situation in a market where the supply and demand for a good or service are in balance at a specific point in time. In this state of equilibrium, the quantity supplied equals the quantity demanded, and market prices and quantities remain constant.

Key characteristics of static equilibrium include:

1. No changes in market conditions: In a static equilibrium, market factors such as consumer preferences, technology, or external events remain constant. There are no shifts in these factors that would affect supply or demand.

2. Quantity supplied equals quantity demanded: The quantity of a product that producers are willing to supply matches the quantity that consumers are willing to buy. This balance results in a stable market price.

3. Stable prices and quantities: Prices and quantities in the market do not change, at least for the moment. There is no inherent tendency for them to adjust because market conditions are assumed to be fixed in the short term.

It's important to note that static equilibrium is a simplified concept used in economic analysis to make initial assessments and models. In the real world, markets are dynamic, and conditions are constantly changing, leading to adjustments over time, which would be described as dynamic equilibrium.

Difference between dynamic and static equilibrium -

Dynamic and static equilibrium are two important concepts in microeconomics that describe different states of an economic system:

1. Static Equilibrium:

- Static equilibrium refers to a situation where the various economic variables, such as prices, quantities, and market conditions, remain unchanged and stable over time.

- In static equilibrium, the economy is at rest, and there are no ongoing changes or fluctuations in economic parameters.

- It assumes that supply and demand are in balance, and there is no inherent tendency for change or adaptation in the system.

2. Dynamic Equilibrium:

- Dynamic equilibrium, on the other hand, is a state where economic variables are in continuous flux and change but in a manner that results in a stable, long-term pattern.

- In dynamic equilibrium, the economic system is not at rest, and it acknowledges that prices, quantities, and market conditions are constantly adjusting due to various economic forces.

- It allows for adaptability and responsiveness to changing circumstances while maintaining a certain level of stability in the fluctuations.

In summary, the key difference lies in the nature of change within the economic system. Static equilibrium assumes a static, unchanging state, while dynamic equilibrium acknowledges that the system is in constant motion but maintains a degree of stability in its fluctuations over time.

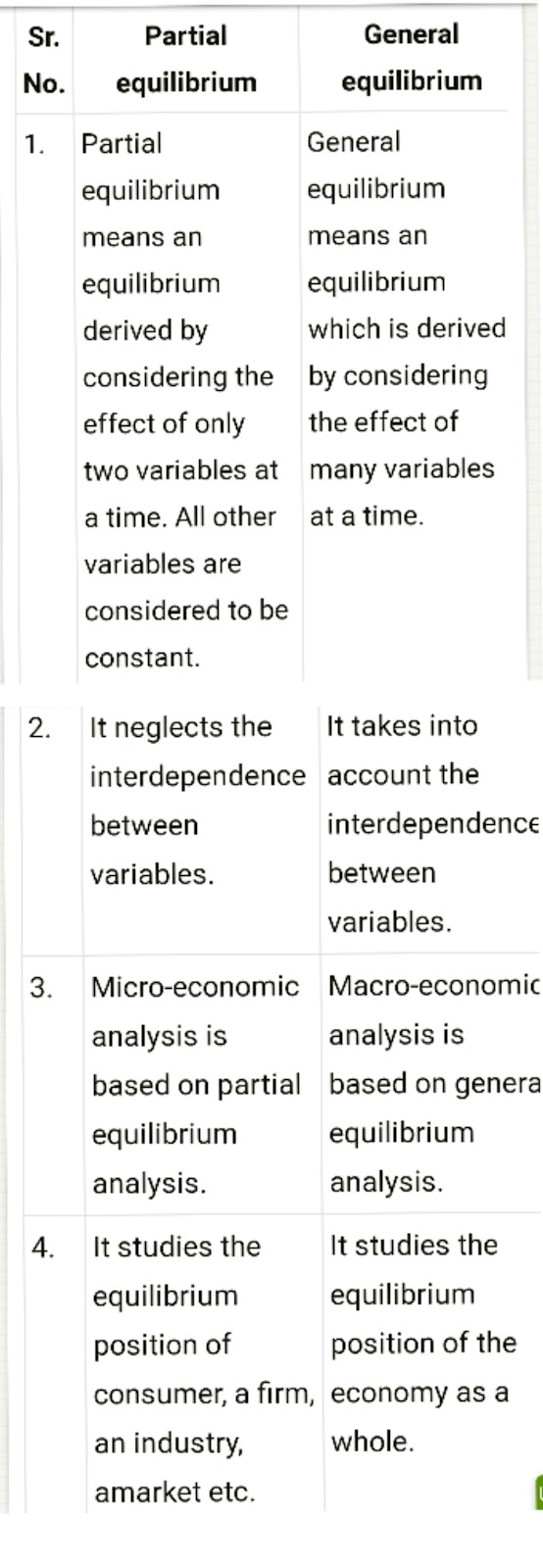

General and partial equilibrium -

General equilibrium -

In economics, general equilibrium theory attempts to explain the behavior of supply, demand, and prices in a whole economy with several or many interacting markets, by seeking to prove that the interaction of demand and supply will result in an overall general equilibrium. General equilibrium theory contrasts with the theory of partial equilibrium, which analyzes a specific part of an economy while its other factors are held constant. In general equilibrium, constant influences are considered to be noneconomic, or in other words, considered to be beyond the scope of economic analysis.[1] The noneconomic influences may change given changes in the economic factors however, and therefore the prediction accuracy of an equilibrium model may depend on the independence of the economic factors from noneconomic ones.

General equilibrium theory both studies economies using the model of equilibrium pricing and seeks to determine in which circumstances the assumptions of general equilibrium will hold. The theory dates to the 1870s, particularly the work of French economist Léon Walras in his pioneering 1874 work Elements of Pure Economics.[2] The theory reached its modern form with the work of Lionel W. McKenzie (Walrasian theory), Kenneth Arrow and Gérard Debreu (Hicksian theory) in the 1950s.

Partial equilibrium -

In economics, partial equilibrium is a condition of economic equilibrium which analyzes only a single market, ceteris paribus (everything else remaining constant) except for the one change at a time being analyzed. In general equilibrium analysis, on the other hand, the prices and quantities of all markets in the economy are considered simultaneously, including feedback effects from one to another, though the assumption of ceteris paribus is maintained with respect to such things as constancy of tastes and technology.

Mas-Colell, Whinston & Green's widely used graduate textbook says, "Partial equilibrium models of markets, or of systems of related markets, determine prices, profits, productions, and the other variables of interest adhering to the assumption that there are no feedback effects from these endogenous magnitudes to the underlying demand or cost curves that are specified in advance."[1] General equilibrium analysis, in contrast, begins with tastes, endowments, and technology being fixed, but takes into account feedback effects between the prices and quantities of all goods in the economy.

The supply and demand model originated by Alfred Marshall is the paradigmatic example of a partial equilibrium model. The clearance of the market for some specific goods is obtained independently from prices and quantities in other markets. In other words, the prices of all substitute goods and complement goods, as well as income levels of consumers, are taken as given. This makes analysis much simpler than in a general equilibrium model, which includes an entire economy.

Consider, for example, the effect of a tariff on imported French wine. Partial equilibrium would look at just that market, and show that the price would rise. It would ignore the fact that if French wine became more expensive, demand for domestic wine would rise, pushing up the price of domestic wine, which would feed back into the market for French wine. If the feedback were included, the higher domestic price would shift out the demand curve for French wine, further increasing its price. This further increase would again raise demand for domestic wine, and the feedback would increase, resulting in an infinite cycle that would eventually dampen out and converge. The importance of these feedback effects might or might not be worth the extra calculations necessary. They will generally affect the exact amount of the original good's price change, but not the direction.

Partial equilibrium analysis examines the effects of policy action only for one good at a time. Thus, it might look at the effect of a price ceiling for luxury automobiles without looking at the effect of that automobile price ceiling on the demand for bicycles, which would be analyzed separately. partial equilibrium applies not just to perfectly competitive markets, but to monopolistic competition, oligopoly, monopoly and monopsony.[2]

Difference between general and partial equilibrium

General equilibrium refers to a situation when the demand and supply of every commodity is equal in the market, whereas, partial equilibrium takes into account a part of the market. Because of partial equilibrium supply and demand of few commodities become equal.

Done by Rohit Joshi....

Must read it too ..

Utility concept and customer demand and market elasticity demand (economics unit 2 by Rohit Joshi )

production possibility , functions and curve and cost , revenue concepts ... specially for B.A. unit 3 by Rohit Joshi

Comments

Post a Comment